How I Almost Lost My Retirement Savings to Fake Senior Fun Investments

I thought I was being smart—finally retiring and looking forward to some fun after decades of work. But what started as harmless entertainment led me straight into a financial trap. I trusted the wrong people, chased shiny offers, and nearly drained my nest egg. This is my story of how senior entertainment scams target retirees, the red flags I missed, and what I learned the hard way. You’re not alone if you’ve been tempted. Many retirees, after years of disciplined saving, feel they’ve earned the right to relax, socialize, and enjoy life. That desire is natural—and it’s precisely what fraudsters exploit. These scams don’t come with flashing warning signs. Instead, they arrive wrapped in dinner invitations, cruise brochures, and promises of community. The danger isn’t in the fun itself, but in the subtle shift from leisure to high-pressure sales. This article walks through how these schemes operate, how to spot them, and—most importantly—how to protect your hard-earned savings without sacrificing the joy of retirement.

The Sweet Trap: When Retirement Fun Turns Risky

After a lifetime of working, budgeting, and putting family first, retirement felt like a long-overdue reward. I wanted to travel, meet new people, and finally enjoy the time I had saved for. That’s when the invitations started arriving—elegant envelopes promising exclusive dinner cruises, wine tastings, and weekend retreats tailored for seniors. They sounded delightful, even glamorous. I didn’t see them as threats. In fact, they felt like recognition—proof that I belonged to a new chapter of comfort and connection. But what I didn’t realize was that these events were not just social gatherings. They were carefully orchestrated entry points into high-pressure financial sales environments.

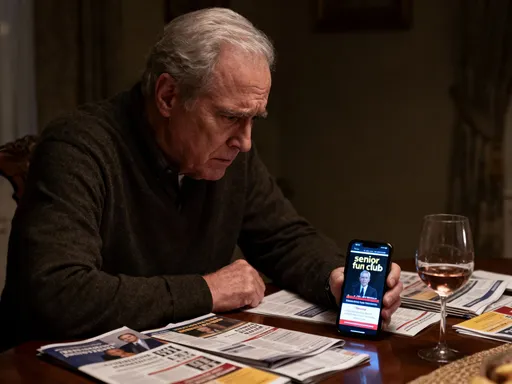

At first, everything seemed perfectly normal. I was greeted warmly, seated at a beautifully set table, and introduced to others who, like me, were enjoying their retirement. The conversation flowed easily—about grandchildren, travel dreams, and the simple pleasures of slowing down. Then, halfway through dessert, the tone shifted. A well-dressed speaker took the stage, thanking us for coming and reminding us how lucky we were to have reached this stage of life. But, he added, luck isn’t enough. Security is what really matters. That’s when the pitch began—not for another cruise, but for a “lifetime income” investment opportunity that would “protect” my retirement savings from market volatility.

What made it so convincing wasn’t the product, but the setting. Because I was already relaxed, surrounded by friendly faces, and enjoying a pleasant evening, my natural skepticism was dulled. The presentation was slick, full of charts that looked official and testimonials from people who claimed to have doubled their monthly income. They used words like guaranteed, secure, and exclusive—terms that resonate deeply with retirees who’ve worked hard to avoid risk. I felt flattered to be included in such a “limited” offer. Only later did I learn that these events were not selective at all. They were mass-marketed to thousands of seniors through mailing lists bought from third parties. The intimacy was manufactured. The urgency was intentional. And the real goal was not my enjoyment—but my wallet.

The Hidden Cost of “Free” Entertainment

One of the most effective tools used in these scams is the promise of something for nothing. Free meals, gift cards, weekend getaways—these perks made the events feel like rewards rather than business meetings. I attended a two-day retreat at a lakeside resort that promised relaxation, light entertainment, and a chance to meet financial experts in a no-pressure environment. The brochure even stated, “No sales pitches—just great company and great views.” But within two hours of arrival, we were ushered into a conference room for a “financial wellness session” that lasted over 90 minutes.

The session was led by a man who introduced himself as a retirement planning specialist. He spoke with confidence, wore a badge that looked official, and used simple language to explain complex financial instruments. He didn’t mention fees, surrender charges, or liquidity restrictions—just the benefits. He described a fixed-index annuity as a “safe harbor” for retirement funds, promising steady growth without market risk. What he didn’t say was that the product came with a 10-year surrender period, high administrative fees, and a commission structure that paid him handsomely for every contract signed. I was inches away from signing because it felt like the responsible choice—until I remembered a rule my son once shared: “If it sounds too good to be true, ask who’s getting paid, and how.”

The real cost of “free” entertainment isn’t just the money you might lose if you invest. It’s the erosion of trust, the confusion, and the pressure to make decisions without proper time or information. These events are not charity. They are funded by the commissions generated from the investments they sell. Every meal, every gift, every scenic view is paid for by the financial products pushed at the end of the night. When something is labeled “free,” it’s essential to ask: What’s the catch? In this case, the catch was a high-cost, low-liquidity financial product disguised as a retirement safeguard. The experience taught me that legitimate financial advice doesn’t come with a complimentary dinner. It comes with time, transparency, and the freedom to walk away.

The Psychology Behind the Pitch

What makes these scams so effective isn’t just the product—they’re built on a deep understanding of human psychology, especially the emotional landscape of retirement. After years of routine and responsibility, many retirees face a shift in identity and social connection. Loneliness, uncertainty about the future, and a desire to feel valued can make even the most cautious person vulnerable. Scammers don’t see victims—they see opportunities shaped by emotion, not logic.

The salespeople at these events aren’t trained in finance; they’re trained in influence. They use techniques rooted in behavioral psychology: building rapport quickly, creating a sense of belonging, and triggering fear of missing out. One man I met called himself a “retirement lifestyle advisor.” He wasn’t registered with any financial regulatory body, yet he spoke with the authority of a seasoned expert. He shared personal stories—about a client who lost everything in the stock market, another who outlived their savings, and a third who found peace through his “exclusive program.” These stories weren’t data—they were emotional hooks designed to bypass rational thinking.

He also used scarcity tactics: “This offer is only available tonight,” “Only 12 spots left,” “You have to act now to lock in these rates.” These phrases trigger urgency, which suppresses critical thinking. When the brain feels pressured, it defaults to instinct, not analysis. I felt it myself—the flutter of excitement mixed with fear. What if I missed this chance? What if this was the one opportunity that could secure my future? That’s exactly what they wanted me to feel. Real financial professionals don’t operate on urgency. They understand that retirement planning is a process, not a performance. They provide documents in advance, encourage questions, and respect your timeline. The moment someone tries to rush you, that’s not enthusiasm—that’s manipulation.

Spotting the Red Flags Before It’s Too Late

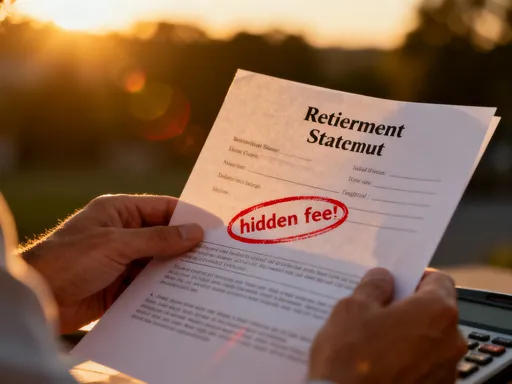

In hindsight, the warning signs were visible, but in the moment, they were easy to overlook. The first red flag was the promise of guaranteed returns. No legitimate investment can guarantee high returns without risk. Even government-backed bonds carry inflation risk. When someone claims you can earn 7% or 8% annually with “no downside,” that’s a major warning. Markets fluctuate. Any product that claims to eliminate risk while delivering strong returns is either misleading or hiding fees and restrictions.

Another red flag was the pressure to decide immediately. I was told that if I didn’t sign that night, the special rate would expire, or the program would be full. Real financial planning doesn’t work on deadlines. You should always have time to review contracts, consult your family, or speak with an independent advisor. Reputable firms send materials in writing, allow cooling-off periods, and never penalize you for waiting. If you’re being rushed, it’s because the seller benefits more from your quick decision than you do.

A third warning sign was confusing language. The presenter used terms like “indexed performance,” “tax-deferred growth,” and “lifetime income rider,” but when I asked for clarification, the answers were vague or circular. I didn’t feel empowered—I felt confused. That’s a tactic. If you can’t explain a product in simple terms, you shouldn’t invest in it. A legitimate advisor will take the time to make sure you understand every detail, including fees, withdrawal rules, and potential penalties. They won’t make you feel silly for asking questions. In fact, they’ll encourage them.

How to Protect Your Nest Egg Without Missing Out

Enjoying retirement doesn’t mean shutting yourself off from social events or new experiences. The goal isn’t isolation—it’s awareness. I still attend gatherings, but now I go with a different mindset. If an event is hosted by a financial company or includes a “financial discussion,” I do research beforehand. I check whether the speaker is registered with the Securities and Exchange Commission (SEC) or the Financial Industry Regulatory Authority (FINRA). A quick online search can reveal disciplinary history, licenses, or customer complaints.

I also bring a simple rule: No signing on the spot. No matter how compelling the offer, I wait at least 48 hours. That cooling-off period gives me time to reflect, talk to my financial advisor, and read the fine print. I’ve learned that legitimate opportunities don’t vanish in two days. If an offer disappears that quickly, it was never real to begin with.

Another strategy is to separate leisure from financial decisions. There are many senior clubs, travel groups, and community events that have no financial agenda. These are the ones worth investing time in—because they enrich life without risking your savings. When an event blurs the line between fun and finance, I ask myself: Is this about connection, or conversion? If the goal is to get me to buy something before the night ends, I politely decline. True enjoyment shouldn’t come with a sales quota.

Building a Defense: Tools and Habits That Work

After my close call, I realized I needed more than caution—I needed a system. I started by creating a financial buddy arrangement with my neighbor, a retired school counselor. We agreed to review any suspicious offers together. It’s not about distrust—it’s about having a second set of eyes. Two people are less likely to be swept up in emotion than one. We share brochures, compare notes, and call each other before making any financial move. It’s become a routine that adds both safety and connection.

I also updated my legal documents. I reviewed my power of attorney to ensure it included safeguards—like requiring dual signatures for large withdrawals or new investments. I set up transaction alerts on my bank and brokerage accounts so I’m notified of any activity. These small steps don’t prevent scams alone, but they create layers of protection. If someone tries to access my accounts without my knowledge, I’ll know immediately.

Most importantly, I invested in knowledge. I took a free retirement planning workshop offered by a local credit union. It covered basics like asset allocation, risk tolerance, and how to read a prospectus. I didn’t need to become a financial expert—just informed enough to spot inconsistencies. Now, when someone uses jargon I don’t understand, I ask for a plain-English explanation. If they can’t provide one, I walk away. Knowledge isn’t just power—it’s peace of mind.

Turning Pain Into Power: A Second Chance at Smart Retirement Living

I didn’t lose everything, but the experience left a mark. It wasn’t just about the money I nearly gave away—it was about the trust I misplaced and the confidence I lost. For a while, I questioned every decision, every invitation, every friendly face. But over time, I realized that shame doesn’t help. Sharing does. That’s why I’m telling my story. Because if one person reads this and pauses before signing a contract, then the pain had purpose.

Protecting your retirement isn’t just about choosing the right investments. It’s about preserving your independence, your dignity, and your peace of mind. True security comes not from chasing high returns, but from making informed, deliberate choices. It comes from knowing your value isn’t tied to how much you spend or how exclusive an offer sounds.

Today, I still enjoy dinner cruises and travel clubs—but on my terms. I go for the company, the views, the laughter. I say no without guilt. I ask questions without fear. And I’ve rediscovered a deeper kind of freedom: the freedom to enjoy life without funding fraud. Retirement should be a season of fulfillment, not fear. By staying alert, informed, and connected, you can protect your nest egg—and still have fun doing it.